Rich Pahls on Nebraska Taxes

Voice from the Grave

Update II: Nebraska Examiner takes notice of same problem (https://nebraskaexaminer.com/2024/06/10/everybodys-got-to-play-breaking-down-nebraskas-more-than-100-sales-tax-exemptions/)

Update: Pahl’s document can now be downloaded from Dropbox at

Short link at https://tinyurl.com/mr9yfz6p

Rich Pahls was a Nebraska State Senator and died a few years ago (https://en.wikipedia.org/wiki/Rich_Pahls). When one of his colleagues offered a tax exemption, I told Pahls to oppose it and a discussion ensued. I presume others told him the same and he put out a paper on the topic from about 2009. I saved it as PDF but replicate it here. God bless Rich Pahls. Special thanks to Kathy Holkeboer, of the Voter Information Project (https://www.voterinformation.org/) for prodding me to trace down this very important document.

Repeal Sales Tax Exemptions and Eliminate or Lower Other Taxes and Fees

Information Packet

Senator Rich Pahls

State Capitol

Lincoln, NE 68509

402/471-2327

rpahls@leg.ne.gov

The Big Picture:

Why Tax Exemptions Make a Big Difference

Our three big taxes in Nebraska are property taxes, income taxes,and sales taxes. How much does each raise annually?

Property taxes: $2.5 billion

Who pays?: All property owners

Who sets the rates?: Local governments

Who collects? Local governments (state government gets

nothing)

Who spends? Local governments (state government gets

nothing)

Income taxes: $2 billion

Who pays?: Income earners

Who sets the rates?: Legislature

Who collects? Department of Revenue

Who spends? Legislature

Sales taxes: $2 billion

Who pays?: Certain buyers

Who sets the rates?: Legislature and local governments

Who collects? Department of Revenue

Who spends? Legislature and local governments

Value of sales tax exemptions: $3 billion and growing

You can easily see that if we eliminated sales tax exemptions, we

could use the revenue to completely overhaul our state tax system.

Here are some options: We could eliminate all property taxes and

lower the income tax. We could eliminate the income tax and lower

property taxes. We could lower sales tax rates. We could do a

combination of all the above.

If we didn’t want to eliminate all of the exemptions, but eliminated the

big ones, we would still have enough revenue to make a substantial

impact on other tax rates.

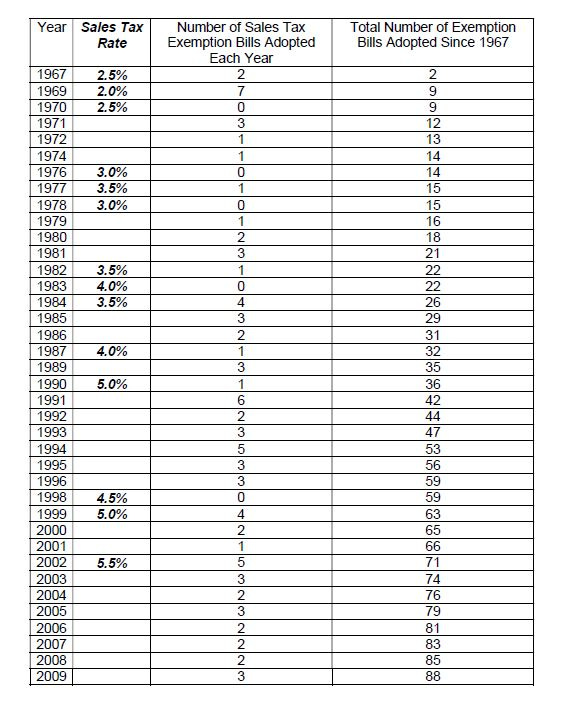

State Sales Tax Rates from 1967 to Today

When the Legislature first enacted a state sales tax in 1967, the

rate was 2.5%.

Today the state sales tax rate is 5.5%. Cities and counties are

authorized to add up to an additional 1.5% on top of the state

rate.

Sales tax exemptions are part of the reason that sales tax rates

have been raised over the years. Each time an exemption is

added, its fiscal impact continues to grow. Over time the sales

tax rates become inadequate--they do not generate the same

amount of revenue--and the Legislature raises the rates again,

rather than going back and closing the loopholes. Certain

groups get exemptions and the remaining taxpayers pick up the

slack through increased tax rates.

Cities and counties that have a sales tax suffer the same loss

and are forced to raise their rates to the maximum 1.5%. Now

we see cities asking the Legislature to raise the maximum local

rate to 2%. In the meantime cities look at raising the tax on

restaurants 4%.

The following chart illustrates the effect exemptions have on the

state sales tax rate. A similar impact occurs on local sales tax

rates. Many bills that were adopted contained more than one

exemption when they passed.

2009 Sales Tax Exemption Legislation Adopted

The 2009 session started out with a total of 15 bills proposing various sales tax exemptions. Three bills passed that created new sales tax exemptions or that expanded current exemptions. The total knownfiscal impact for these three bills is:

FY2009-10: ($158,400)

FY2010-11: ($232,100)

FY2011-12: ($264,900)

FY2012-13: ($292,900)

LB 9 Exempt sales of wood and corn used as fuel and mineral oil applied as a dust suppressant

Fiscal impact (loss to state taxpayers) on the wood and corn portionof the bill

FY2009-10: ($36,400)

FY2010-11: ($38,100)

FY2011-12: ($39,900)

FY2012-13: ($41,900)

Fiscal impact (loss to state taxpayers) on the mineral oil portion ofthe bill:

FY2009-10: ($122,000)

FY2010-11: ($194,000)

FY2011-12: ($225,000)

FY2012-13: ($251,000)

LB 392 Exempt learning communities from paying sales tax

Fiscal impact: unknown. (No fiscal estimate was ever made or

attempted.)

LB 587 Exempt animal grooming services done in conjunction with veterinary

services

No fiscal impact. (This estimate could be disputed. The Department

of Revenue was attempting to collect the tax, but the Legislature

chose to exempt it instead.)

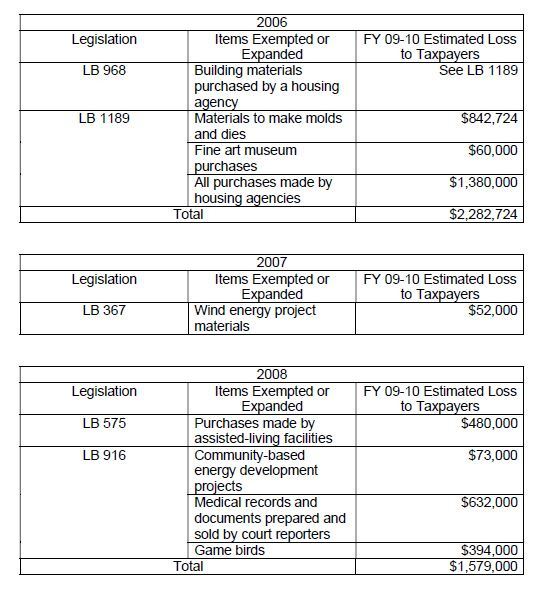

Sales Tax

Exemption Bills Passed in 2006 to 2008

2009 Nebraska Supreme Court Ruling on Sales Tax Exemptions

On June 5, 2009 the Nebraska Supreme Court handed down a ruling

that created another new sales tax exemption. (Concrete Indus. v.

Nebraska Dept. of Rev., 277 Neb. 897)

The Legislature exempted the sale of manufacturing machinery and

equipment in 2005 (but not parts for machinery and equipment). In

2007 Concrete Industries purchased various parts that it used to build

its own manufacturing machinery and equipment. When it purchased

the parts, the Concrete Industries paid sales tax. Concrete Industries

filed a claim with the Nebraska Department of Revenue for a refund,

stating that the purchases should be tax exempt under the law

adopted in 2005 by the Legislature that granted an exemption for

manufacturing machinery and equipment. The Revenue Department

denied the claim. Concrete Industries challenged the Revenue

Department’s decision and the case ultimately moved its way up to

the Supreme Court for a final determination.

In its ruling, the Supreme Court reversed the department’s denial of

the claim and required the department to refund the sales tax to

Concrete Industries. The court, in its ruling, said, “…it would make

very little sense to exempt assembled machinery from sales and use

taxes, and to exempt each and every part of that machinery from

sales and use taxes if it is purchased to replace an original part, but

to impose a tax on the purchase of the same parts when they are

purchased to assemble the machinery in the first place.” (page 905)

“We hold that…the “sale . . . of manufacturing machinery and

equipment” includes the sale of items that are assembled to make

manufacturing machinery and equipment.” (page 906)

As a result of this ruling we can now add an additional sales tax

exemption to the list started by the Legislature.

If the Legislature continues down the road of granting more

exemptions we place our Department of Revenue in a precarious

position. This past session some senators criticized the Department

for not collecting sales tax in some areas. Then the Legislature

turned around and passed legislation to grant the exemption.

In the Concrete Industries case the Department tried to make sense

of the various loopholes the Legislature created and it sought to

collect the tax. The Court considered all the loopholes the Legislature

created and said it didn’t make any sense to grant exemptions on

manufacturing machinery and equipment but not on the individual

parts if a company chose to buy the parts individually and construct

its own equipment. What’s next?

It’s bad enough when the Legislature grants exemptions, but now we

have put our Supreme Court in the position of granting them. The

Legislature needs to take back its responsibility from the court and

close these loopholes. We do not know the cost of this ruling yet.

Supreme Court opinions don’t come with fiscal estimates.

While taxes and the exemptions are a big deal per the article. The bigger problem in my opinion is spending. So many people/organizations have their tin cup out rattling it for dollars that the state cannot or will not say NO! These panhandlers use the compassion argument to justify their state enforced theft.

Once the government is enlisted to be the muscle in this theft ring the theft never stops. We have all heard and said taxes are too high since we entered the workforce. Very seldom is spending attacked, its always justified for the children, for this or that. These groups recruit government to be their thugs, they don't have the brass to steal on their own so they recruit government to do their thuggery work.

We've all heard the emotional arguments justifying this theft. I counter - Can anyone tell me what is compassionate about stealing from one at the point of a gun and giving to another?